In today’s rapidly evolving business landscape, staying ahead of the competition requires more than just a great product or service. It demands a deep understanding of the market, consumer behavior, and emerging trends. This is where the market research process becomes invaluable. In this blog post, we will delve more into market research and explore...

There is never a wrong time to do market research. However, most research projects are birthed because a company or organization is at a crossroads. Whether you’re a startup or Fortune 500 company, you’ll have critical decisions to make. This blog will detail common market research examples and how our clients have used them to...

Product Development Research For The Banking Industry

Austin Parker

Launching a new banking product is no small feat. From regulatory hurdles to rapidly shifting customer expectations, financial institutions face unique challenges that can’t be solved by guesswork.

Whether you’re considering launching a new type of checking account, a mobile app upgrade, or a premium credit card, success hinges on one thing: knowing exactly what your customers want.

For banks, product development research gives the clarity to move forward with confidence. With the right data, financial institutions can validate ideas, reduce risks, and deliver products that truly align with customer needs.

In this article, we’ll explore what product development research looks like for banks, how it helps institutions stay competitive, and what to expect from the process.

Turn research insights into smarter banking product decisions.

In simple terms, product development research helps banks make smarter, data-backed decisions when creating or refining products.

Instead of relying on gut instinct, it allows you to test ideas with real customers before investing heavily in development.

Done correctly, this type of research helps banks:

Spot market gaps competitors haven’t filled

Validate product concepts before launch

Pinpoint pricing and positioning strategies that resonate

Reduce costly missteps while strengthening customer loyalty

In our experience, the most successful banks use research not just as a checkpoint before launch, but as a continuous feedback loop throughout the product lifecycle.

How Product Development Research Can Help Your Banking Brand

Over the years, working with financial clients, we’ve seen how product development research can transform banking product launches into strategic wins.

By using real customer feedback for informed decisions, our clients have been able to reduce risk, speed up decision-making, and deliver products that meet the needs of their target audiences.

Here are a few ways it can help as examples:

Validating New Product Concepts Before Launch

The biggest advantage of product development research is the ability to validate ideas before launch. Banks do not have to gamble on whether a new product will resonate.

Instead, they can test concepts with real consumers to see which features are most appealing and which can be removed without hurting adoption. This reduces risk and ensures resources are invested in the right places.

The institution wanted to measure demand for a new digital banking product. Drive Research conducted an online survey with 1,000 respondents and paired it with competitor analysis.

Within just two weeks, the bank had clear evidence of which features customers valued, what gaps existed in the market, and how to position the offering to stand out. With these insights, leadership could move forward with confidence knowing the product was designed around actual customer needs rather than assumptions.

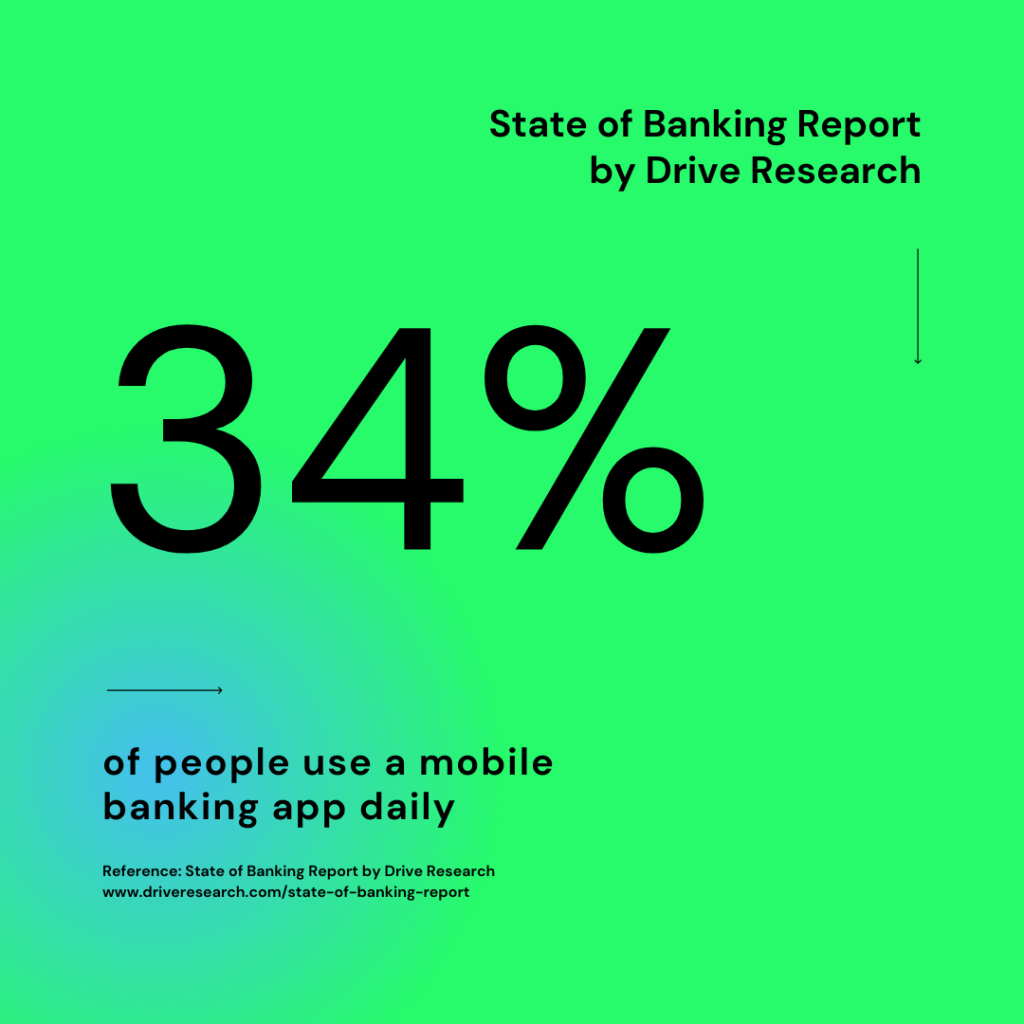

Optimizing Mobile Banking Features

Mobile banking has become a daily habit for many customers. In fact, according to our survey of 1,000 banking consumers, 34% of people use their mobile banking app every single day. With that level of engagement, investing in the right features is critical.

Product development research helps banks identify which tools customers value most, whether that is bill pay, instant account alerts, or other high-impact functions.

By focusing development resources on the features that drive the most use, banks can increase retention and avoid spending on upgrades that would go largely unnoticed.

Fine-Tuning Product Pricing

Pricing can make or break most products. For instance, a premium savings account might only succeed if the interest rate feels competitive.

Running a pricing research study allows banks to identify the sweet spot where customers see value without eating into margins.

Beyond rates, this research can also uncover what minimum balance requirements, account fees, or added perks are most acceptable to different customer segments.

With this insight, banks can design products that feel both attractive and fair, while still protecting profitability.

Sometimes the challenge is not launching something new but improving a product that already exists.

Underperforming accounts, loans, or services often fail for reasons that research can reveal. Issues like unclear eligibility rules, confusing terms, or a clunky application process can easily drive customers away before they ever sign up.

We find that Voice of Customer research for financial services is particularly valuable here. By collecting direct feedback from customers, banks can identify the specific friction points holding products back and make targeted adjustments.

Even small changes to product design or communication can significantly improve conversions and strengthen customer relationships.

What to Expect From a Product Development Research Project

While every study we conduct is customized, the research process typically follows a series of steps. These are the same steps we use with our banking clients, and they are also the best practices we recommend following if your institution chooses to work in-house or with another firm.

1. Prep

This phase is about alignment. Banks should start by defining which products or concepts need testing, along with the goals for the project.

Common scenarios include:

Validating a new lending product

Testing a mobile app feature

Repositioning an existing checking account product

It is also important to clarify which audiences to engage, such as current customers or members, small business owners, or prospective account holders, etc.

2. Project Setup

Once objectives are clear, the next step is to design the research approach.

This means choosing the right methodologies (surveys, focus groups, interviews), drafting unbiased questions, and confirming sample criteria.

For banks, it is especially important that all materials align with compliance requirements and avoid misusing or exposing customer data.

Even if you are running the project internally, take time to ensure the design is ethical, compliant, and representative of your target audience.

Once the design is finalized, the focus shifts to execution. This stage is about reaching the right people and ensuring their feedback is captured in a secure and reliable way.

For financial institutions, that often means working with vetted panels or recruiting customers through official bank channels rather than relying on open links that could invite fraudulent responses.

Throughout the process, strict safeguards should be in place to protect customer privacy and comply with regulations such as GLBA.

4. Data Cleaning

Raw data is rarely ready to use. In this step, invalid or incomplete responses are removed, quotas are verified, and inconsistencies are corrected.

While some organizations overlook this step, in banking, it is non-negotiable. Making decisions with flawed data can create compliance risks, financial losses, and reputational damage.

Clean, reliable data ensures leadership has a trustworthy foundation for decision-making.

Here are the data cleaning steps we follow on every project to ensure results are accurate and reliable.

5. Reporting

The final step is turning data into actionable insights. Our data analysis is aimed at answering your initial questions with clear visuals, executive-level summaries, and data-driven recommendations.

In many of our banking studies, this often means connecting the dots between customer feedback and product performance, pricing strategy, or regulatory positioning.

For example, here are some insights a product development report might reveal to a bank:

Feature prioritization: Customers rank mobile check deposit and account alerts as “must-have” features, while peer-to-peer payment tools are seen as “nice-to-have.”

Pricing thresholds: The optimal balance requirement for a premium savings account is $1,000, with diminishing interest beyond $2,500.

Market positioning: Younger customers perceive bundled accounts with digital perks as more attractive than those centered on traditional rewards.

Regulatory considerations: Confusion around fee disclosures is creating mistrust, signaling the need for clearer communication to stay compliant.

The best reports do more than answer what happened, they explain why and recommend what to do next.

Validate your new banking product with our custom research services.

Why Accurate Data is so Crucial For Product Development Research in Banking

When it comes to product development, mistakes are costly. Launching a misaligned product can lead to wasted resources, regulatory headaches, and even loss of customer trust. This is why accuracy is essential.

The Risks of Inaccurate Data

If your data is flawed, say from biased survey questions or unrepresentative samples, you risk making the wrong decision with confidence. That might mean prioritizing features no one uses, overestimating demand, or misjudging customer willingness to pay.

Why Accuracy Matters More in Banking

Banking is built on trust. Unlike retail or consumer goods, a failed banking product doesn’t just hurt short-term sales, it can damage long-term relationships and open the door to competitors.

Customers want financial products that feel fair, transparent, and worth their investment. Research ensures your offerings meet those expectations.

In fact, our State of Banking report shows that when learning about new banking products, consumers rely most on official websites, online search, and recommendations from friends and family.

This means that if a product misses the mark, word spreads quickly through the same trusted channels customers turn to when evaluating their options.

Download the State of Banking Report

Explore the data, trends, and takeaways shaping the future of finance.

"*" indicates required fields

Turning Accuracy into ROI

Accurate research pays for itself time and time again.

By prioritizing the right features, setting profitable pricing, and crafting messaging that resonates, banks not only launch more successful products but also strengthen retention and loyalty.

Product development research is more than a safeguard against failed launches—it’s a competitive advantage. In a crowded market, the banks that listen to their customers and adapt quickly are the ones that win.

Whether you’re considering a new product, optimizing an existing one, or simply exploring opportunities for growth, research gives you the clarity to move forward with confidence.

Ready to see how product development research can guide your next big banking initiative?

We analyze more than data—we also track how our site is used to improve your experience. Cookies help us understand what’s working so we can deliver the most relevant insights. Click “Accept” to enable full functionality.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.