In today’s rapidly evolving business landscape, staying ahead of the competition requires more than just a great product or service. It demands a deep understanding of the market, consumer behavior, and emerging trends. This is where the market research process becomes invaluable. In this blog post, we will delve more into market research and explore...

There is never a wrong time to do market research. However, most research projects are birthed because a company or organization is at a crossroads. Whether you’re a startup or Fortune 500 company, you’ll have critical decisions to make. This blog will detail common market research examples and how our clients have used them to...

Measuring your Credit Union’s NPS in Short: Net Promoter Score (NPS) helps credit unions measure how likely members are to recommend them to others. It is one of the simplest ways to track member loyalty, satisfaction, and early signs of frustration. While financial services organizations often average around +30 to +40, many credit unions should aim for +50 or higher. The real value, though, comes from understanding why members gave the score they did and using that feedback to improve the member experience.

How likely are members to recommend your credit union to a friend or family member?

It seems like a simple question, but for credit unions, the answer can reveal a lot.

Many members will not tell you directly when they are frustrated. They may not complain about a confusing loan application or poor mobile banking experience. Instead, they quietly move more of their banking relationships elsewhere.

Net Promoter Score gives you a clear way to measure member loyalty while also uncovering what is helping (or hurting) their overall experience.

For example, your credit union may have a strong overall NPS, but the open-ended feedback could show that members who recently applied for a mortgage are less likely to recommend your credit union because communication slowed down after their application was submitted.

By tracking and improving your credit union’s NPS, you’re not only boosting member satisfaction in the short-term, but you’re also creating relationships that drive referrals, retention, and growth for the long haul.

Uncover what drives customer loyalty with expert-led NPS surveys

For credit unions, NPS is more than just another customer satisfaction metric. It is a direct measure of member experience, loyalty, and satisfaction. With more members comparing digital tools, fees, and personalized service across financial institutions, understanding where your credit union stands has never been more important.

Every NPS survey centers around this one question:

“On a scale of 0 to 10, how likely are you to recommend [Credit Union Name] to a friend, family member, or colleague?”

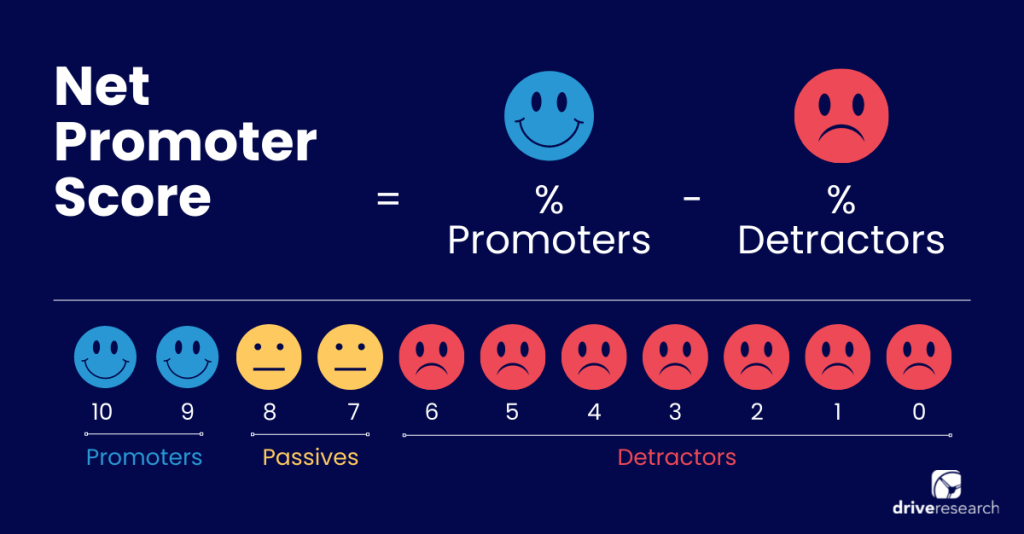

The responses are grouped into three categories:

Promoters (9–10): Your most loyal members. They actively recommend your credit union and help fuel growth through word of mouth.

Passives (7–8): Members who are generally satisfied but not enthusiastic enough to promote your credit union. They may be vulnerable to switching.

Detractors (0–6): Members who are unhappy or frustrated. Without action, they’re likely to leave and may even share negative feedback with others.

One reason NPS is so popular with credit unions is its simplicity. As member expectations continue to evolve, credit unions don’t always have the time or resources to analyze dozens of complex member experience metrics.

So, NPS provides a streamlined pulse check that cuts through the noise while the follow-up feedback provides the meaningful context of where the real value lies, all without spending extra time and money getting lost in disconnected data.

How To Calculate NPS For Credit Unions

To calculate NPS, members are asked:

“How likely are you to recommend [Credit Union Name] to a friend or family member?”

And it’s calculated using the following formula:

NPS = % of Promoters – % of Detractors

For example, if 70% of members are Promoters and 20% are Detractors, your credit union’s NPS would be +50.

Passives are not included in the calculation, but they should not be ignored.

A large number of Passives may mean your members are satisfied enough to stay, but not loyal enough to recommend you.

For credit unions, that distinction is important. A member who gives a 7 or 8 may still use your checking account, but they may not think of your credit union first for a mortgage, auto loan, credit card, or small business account.

How often should credit unions measure NPS?

Most credit unions should measure NPS at least once or twice per year, but quarterly pulse surveys are recommended as they provide more actionable and timely insights. More regular measurements help track member sentiment during times when business may change, and identify emerging issues quickly.

The Key Takeaway: With your responses, by thinking of your NPS score as a roadmap rather than a final grade, you can move beyond the number itself and focus on the member feedback that connects to the bigger scope of your business goals and make efficient, actionable strategies that drive smarter decisions.

Why Credit Unions Should Measure NPS

Member recommendations have always been weighty for credit unions. Our recent data shows that 50% of people trust guidance from their friends and family over traditional advertising.

At the same time, we also found people are turning to online reviews more rapidly than ever, with 18% of banking consumers turning to social media for financial advice – that number more than doubles for Gen Z (44%).

By measuring NPS, credit unions can understand what drives these recommendations straight from the people who matter most: their members.

Useful resource: Interested in seeing more insights from our survey of 1,000 banking consumers? Download our State of Banking Report.

Reason #1: To Measure Member Loyalty

Studies have proven that brand loyalty is on the rise, with 59% of customers being willing to refer brands they like to their family and friends. For credit unions, that loyalty often translates into word-of-mouth recommendations from happy members which may be one of the most valuable forms of marketing.

At the same time, loyalty shouldn’t be taken for granted. In our same study, 37% said they’re willing to make the change if another institution better meets their needs. Younger generations, in particular, are leading this shift.

For credit unions, this is where measuring consumer loyalty is especially important because their biggest threat isn’t losing members entirely.

It’s remaining their “secondary” financial institution, or even an afterthought until a member finally makes the change. They may be actively expanding their banking relationships through other products and services until they’re ready to completely move.

By tracking NPS, credit unions can put a number on loyalty and get a clearer picture of which relationships may need attention before members shift their attention elsewhere:

Promoters (those who give a 9 or 10) are your biggest influencers and will actively spread the word and deepen relationships.

Passives may be satisfied and will continue banking with you, but may not feel inspired enough to recommend you yet or look elsewhere for services.

Detractors highlight areas where service may be falling short and increase the risk of members taking their business to another institution.

Reason #2: Gather Reasons for Dissatisfaction and Identify areas to Improve

One of the biggest strengths of NPS surveys is that they capture both numbers and stories, also known as qualitative and quantitative data. In the financial services world, this is a significant edge for institutions as they are able to see beyond the numbers they work with daily.

From our past research, we’ve found that asking a simple follow-up like:

“Please explain why you gave [Credit Union Name] this score,” you uncover the real reasons behind member satisfaction (or dissatisfaction).

This insight gives you a clear path for what services require your attention more than others.

For example, you may discover that mortgage borrowers consistently rate lower than checking account members, signaling pain points in home loan servicing. With this insight, your team can prioritize improvements where they’ll make the most impact.

Reason #3: Align Business Plans with Member Expectations

When it comes to expectations of features and more functional improvements, measuring NPS is invaluable for learning the everyday things that can make your members’ overall experience better.

Asking follow-up questions like, “What can we do to make your experience better?” lets members share their expectations directly.

From this question, maybe your members will mention faster mobile deposits, easier loan applications, or more financial education workshops. Whatever the case, these responses guide your credit union in aligning business plans with what members care about most.

Reason #4: To Reduce Member Churn Rate

For most financial institutions, churn rate, also known as attrition, refers to the number of customers who’ve left your bank or credit union in a certain period due to a bad experience.

The worst part? This rarely happens without warning, and rarely affects just one account.

Retaining an existing member can be more valuable than replacing one. A member that leaves not only signals lost deposits now, but also takes future business with them, meaning institutions miss out on everything from potential loans to credit cards.

Intervening on that loss now with NPS as an early warning system allows you to dig deeper, identify detractors, address concerns long before dissatisfaction spreads, and protect your bottom line.

Find satisfaction gaps before they cost your credit union members

Credit unions have always had a unique advantage when it comes to member satisfaction because they are handling a major thing that stays top of mind for many people: finances.

They understand that when it comes to money, strong relationships and community engagement create loyal members from the get go.

But expectations are changing.

While members still value personal service, they also want experiences that feel even more seamless and streamlined than what national banks offer. This means faster loan approvals, intuitive mobile banking, and even digital features that motivate their financial wellness are more crucial than ever.

In our experience, the biggest gains don’t come from one major change.

Rather, they are the result of several, smaller strategic moves across customer experience. Here’s where you can start:

A low NPS signals an ongoing problem within your member experience ecosystem. From tellers to loan officers to leadership, ensure your entire team understands why NPS matters and how their role contributes to member satisfaction.

Learn from your biggest advocates. Get insights from members who give you a 9 or 10 on the NPS scale and see what they value most and double down on those strengths.

Passives (7s and 8s) are satisfied but not loyal. But don’t ignore them! Instead, ask them what’s missing. Often, small changes (like improving mobile features, offering quicker loan approvals, or reducing paperwork) can convert them into enthusiastic promoters.

Level up front-line communication. Human touch is key within credit unions, so train staff to deliver consistent, empathetic, and personalized service whether in-branch, over the phone, or online.

Leverage technology that emphasizes customer investment. Members expect mobile banking, instant transfers, and 24/7 account access. Utilizing modern digital solutions shows that you value their time and keeps you competitive with larger banks and fintechs.

Useful Resource: Check out our guide on 10+ Ways to Improve Your NPS Over Time for more strategies to strengthen member experience and turn more members in your advocates.

What is a Good NPS Score for Credit Unions?

There isn’t one perfect benchmark since member expectations can vary depending on market and institution. That being said, the financial services industry averages around +30 to +40. Many successful credit unions aim for scores above +50, while scores above +70 signal exceptional loyalty and member satisfaction.

NPS Score

What It Generally Means

Also Ask Yourself..

Below 0

More detractors than promoters.

How do I identify the biggest sources of member dissatisfaction?

0-30

Loyalty is developing, but there is room for improvement.

Which improvements can we prioritize now to start solving recurring frustrations?

30-50

Around the industry average.

Which passives can we convert into promoters?

50-70

Strong member loyalty and satisfaction.

Which improvements have had the greatest impact over the year, and how can we optimize them more?

70+

Exceptional member advocacy.

Which parts of the member experience should we continue monitoring to sustain results?

A high NPS is encouraging, but the comments behind the score are what help your credit union improve. A lower score is not automatically bad if it gives your team the insight needed to fix issues and prevent future attrition.

The best NPS benchmark is your own score over time.

Are you improving?

Are specific member segments becoming more satisfied?

Are fewer members mentioning the same recurring pain points?

Those answers are often more useful than comparing your score to a broad industry average.

Measuring NPS is simple. Knowing what to do with the results is where many credit unions need more support.

Drive Research helps credit unions design, field, and analyze member NPS surveys that go beyond a single score. Our team can identify which member segments are most satisfied, where dissatisfaction is building, and what changes are most likely to improve loyalty, referrals, and retention.

Whether your credit union wants to benchmark member experience, understand why members are leaving, improve digital banking satisfaction, or track loyalty over time, our team can build a custom NPS survey around your goals.

Uncover what is driving member loyalty and where satisfaction gaps may be costing your credit union growth.

4 Critical Surveys for All Banks and Credit Unions

Blog Posts

8 Member Survey Questions for Your Credit Union

When You Give Us A Cookie

We analyze more than data—we also track how our site is used to improve your experience. Cookies help us understand what’s working so we can deliver the most relevant insights. Click “Accept” to enable full functionality.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.