In today’s rapidly evolving business landscape, staying ahead of the competition requires more than just a great product or service. It demands a deep understanding of the market, consumer behavior, and emerging trends. This is where the market research process becomes invaluable. In this blog post, we will delve more into market research and explore...

There is never a wrong time to do market research. However, most research projects are birthed because a company or organization is at a crossroads. Whether you’re a startup or Fortune 500 company, you’ll have critical decisions to make. This blog will detail common market research examples and how our clients have used them to...

NPS for Banks: How to Measure & Improve Your Score

Emily Rodgers

How loyal are your customers really? In banking, trust and satisfaction can make or break a relationship, but many financial institutions overlook one of the simplest ways to measure both.

Net Promoter Score (NPS) has become a go-to benchmark for leading companies in every industry, helping them understand not just how satisfied their customers are, but whether those customers are likely to recommend them to others. For banks, that insight can be transformative.

In this article, we’ll explore why measuring NPS matters so much for financial institutions and what it reveals about customer loyalty, retention, and growth potential.

Measure your bank's NPS and gain actionable insights to enhance customer loyalty with our market research company.

Net Promoter Score (NPS) is a customer loyalty metric that measures how likely people are to recommend your bank to friends, family, or colleagues. It goes beyond traditional satisfaction surveys by showing whether customers are not just content, but actually willing to advocate for your brand.

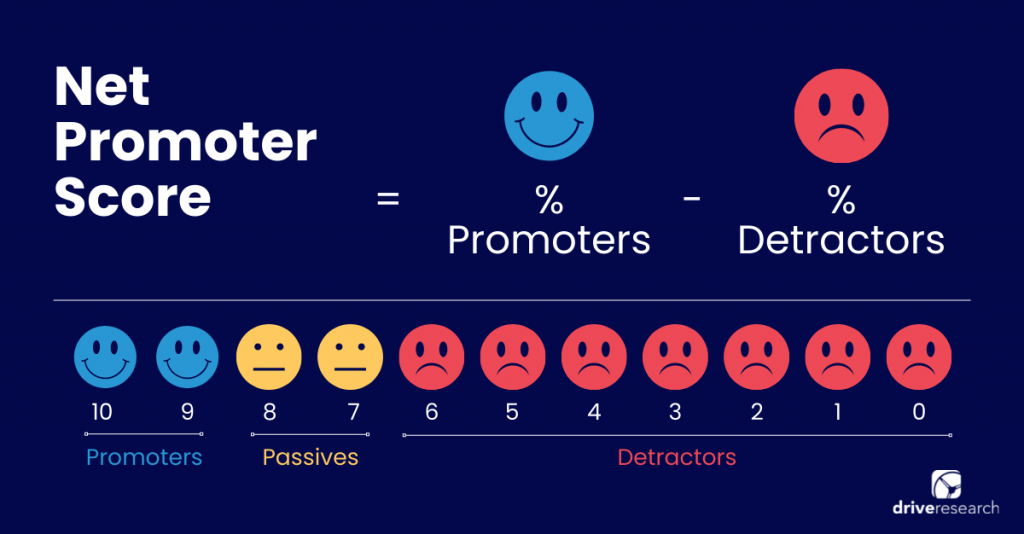

NPS is calculated based on one question: “On a scale of 0 to 10, how likely are you to recommend [BANK NAME]?”

Customers who score a 9 or 10 are considered Promoters.

Those who score a 7 or 8 are Passives.

Those who score 0 to 6 are Detractors.

Your final NPS is the percentage of Promoters minus the percentage of Detractors, which results in a score ranging from -100 to +100. The higher the score, the more loyal and satisfied your customers are.

The video below features our team highlight NPS a bit more.

Studies have proven that brand loyalty is on the rise. 59% of customers are willing to refer brands they like to their family and friends, and 66% admit to spending more on brands to which they are loyal to.

As a result of calculating NPS, organizations can quantify member satisfaction and loyalty to help increase business.

Gather Reasons for Dissatisfaction and Identify areas to Improve

The good thing about NPS surveys is that they measure both qualitative and quantitative data. Besides detecting detractors, passives, and promoters, NPS surveys also gather the reasons for customer dissatisfaction.

Our bank market research company always recommends adding a follow-up question after respondents provide their scores.

In an open-ended question, we ask “Please explain why you rate [Bank ABC] a [Insert Score].”

In doing so, you can easily collect customer feedback. It puts the why behind the what.

Additionally, you can use correlation analysis for a deeper understanding of customer satisfaction or dissatisfaction. Perhaps there is a correlation between home loan customers and strong dissatisfaction scores.

This insight gives you a clear path for what services require your attention more than others.

Align Business Plans with Customer Expectations

Measuring NPS will help you identify customers’ expectations in terms of improvements and features. For instance, when you ask a follow-up NPS question like ‘What can we do to make your experience better’ it encourages your customers to share their suggestions.

These suggestions will help you understand your customers’ expectations and align your business plans accordingly.

To Reduce Customer Churn Rate

For most businesses, churn rate refers to the number of customers who’ve left your company in a certain period due to a bad experience. When customers suddenly leave your company, how do you know the reasons for the exit?

When it comes to banking services, it’s all about numbers. So, you’ll need to keep track of the ongoing and incoming customers, and measuring NPS can help you with this.

Download the State of Banking Report

Explore the data, trends, and takeaways shaping the future of finance.

"*" indicates required fields

How to Measure NPS for Banks

Most banks measure NPS as part of a larger customer satisfaction survey, not in isolation. It is measured through one simple question:

On a scale of 1 to 10, how likely are you to recommend [Company Name] to a friend, relative, or colleague?

Then, customers select a number from 0 (not at all likely) to 10 (extremely likely).

Based on their response, they fall into one of three groups:

Promoters (9–10): Loyal customers who are very satisfied and eager to recommend your bank.

Passives (7–8): Neutral customers who are generally satisfied but not enthusiastic enough to spread the word.

Detractors (0–6): Dissatisfied customers who may leave and could discourage others from choosing your bank.

Once responses are collected, calculating NPS is simple:

NPS = % of Promoters – % of Detractors

Example: If 80% of your customers are promoters, 50% are passives, and 20% are detractors, the NPS score, in this case, is 60 (80-20).

What is a Good Net Promoter Score for Banks?

A “good” NPS can vary depending on your industry, but for banks, aiming for a positive score (above 0) is an important starting point. This means you have more Promoters than Detractors.

That said, banks typically benchmark their performance against industry averages. According to customer experience research, the average NPS for banks and credit unions usually falls between 30 and 40.

Here’s how you can interpret your score:

0 to 30: Average, with clear room for improvement.

30 to 50: Strong, showing you’re building loyalty and trust.

50+: Excellent, signaling that customers are not only satisfied but actively recommending your bank.

It’s important to remember that context matters. A score of 40 might be considered great in banking, but just average in another sector like technology. That’s why comparing your NPS to financial services benchmarks is critical to understanding where you stand.

Measure customer loyalty now and benchmark against banking industry competitors.

Improving your score takes more than one department, it requires a bank-wide commitment to delivering better customer experiences. The strategies below are general recommendations any financial institution can apply.

However, if our financial services market research firm were to conduct an NPS survey for your bank, we can provide tailored recommendations based on your specific data and customer insights.

1. Make NPS a shared responsibility If your score is low, it signals a larger issue that everyone should care about. Ensure your entire team understands what NPS means, why it matters, and how their role contributes to improving it.

2. Listen to your promoters Your happiest customers can tell you what your bank does best. Learn what drives their loyalty and use those insights to reinforce your strengths and attract more promoters.

3. Turn passives into promoters Passives aren’t unhappy, but they’re not enthusiastic either. Asking them what would improve their experience can reveal small, actionable changes. Since they’re closer to becoming promoters than detractors, their feedback is especially valuable.

4. Strengthen front-line communication Customer service interactions shape perception. Train staff to provide personalized, empathetic, and efficient service—whether in person, on the phone, or through digital channels. Even small improvements in tone and responsiveness can make a lasting impression.

5. Embrace technology Modern banking customers expect convenience and speed, from mobile apps to online account management.

In fact, in the past year, more than half of consumers completed routine tasks like person-to-person transfers (77%) or mobile check deposits (61%) without ever stepping inside a branch (Source).

Investing in user-friendly, secure digital tools not only meets expectations but also helps your bank stay competitive while improving customer satisfaction.

Understanding your bank’s Net Promoter Score is the first step toward improving customer loyalty and retention. At Drive Research, we go beyond surface-level metrics to deliver in-depth insights tailored to your bank’s unique customer base.

Our team will not only measure your NPS, but also benchmark your results against competitors and provide clear, actionable recommendations to help you turn feedback into meaningful improvements.

Bank & Credit Union Market Research Options for 2026

Blog Posts

4 Types of Banking Customers in 2025 (& How to Reach Them)

When You Give Us A Cookie

We analyze more than data—we also track how our site is used to improve your experience. Cookies help us understand what’s working so we can deliver the most relevant insights. Click “Accept” to enable full functionality.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.